Author Affiliations

Author Affiliations

Abstract

This paper highlights the role of digital technologies in reworking women’s entrepreneurship in Africa, focusing on e-commerce, fintech, and agritech. Digital platforms, such as Jumia and M-Pesa, create avenues for empowering women with increased market access and financial inclusion; these avenues allow women to rise above the traditional constraints of a lack of mobility and a lack of finance. Agritech solutions, such as FarmDrive, help women farmers based on data-driven agricultural practices. Notwithstanding these developments, there are still challenges to encounter, such as the gender digital divide, limited technical skills, and restricted access to capital. This study, therefore, calls for focused digital literacy programs, gender-inclusive policies, and innovative models of finance that have the potential to unlock the full potential of women entrepreneurs in Africa, enabling their contributions toward economic growth to be inclusive.

Keywords

Digital technologies, E-Commerce, Fintech, Agritech, FarmDrive, Women entrepreneurs.

Introduction

Digital technologies play an increasingly critical role in promoting female entrepreneurship across the continent through platforms in e-commerce, fintech, and agritech, which introduce new avenues through which women can participate in economic life. Entrepreneurship has been regarded as masculine, but through the intervention of digital tools, African women bridge the gap in socio-economic bottlenecks: restricted market access, limited financial services, and traditional gender roles.[1] However, e-commerce platforms like Jumia and Takealot have given women the ability to access new markets greater than their local communities, including global trade, amidst their mobility constraints and limited physical infrastructure.[1] In a similar vein, fintech innovations like mobile wallets and digital loans supplied by platforms such as M-Pesa and Paga have been important in improving women’s financial inclusion and addressing some challenges that many women face in accessing credit through conventional banking systems.[2,3] In agriculture, agritech solutions like FarmDrive and Esoko are giving women the power to increase their productive capacity through access to market information, financial services, and new farming tools. Such platforms not only increase productivity but also create opportunities for rural women in the larger economy, making valuable contributions toward bridging economic disparities.[4]

There are some formidable challenges that digital technologies bring. Restricted access to finance, combined with the gender digital divide and low digital literacy levels, creates a barrier for many women entrepreneurs on the continent. Also, coronavirus disease 2019 (COVID-19) widened the inequality gap, as disruptions within women-owned enterprises were more severe and recoveries slower than those in enterprises with male ownership.[1] The targeted policies and innovative financing models are needed to ensure the realization of sustainable and inclusive growth for women entrepreneurs in

Africa.[3]

This paper discusses the ways in which digital technologies are disrupting female entrepreneurship in Africa, placed within the context of e-commerce, fintech, and agritech. It also shows how new digital platforms have enabled women to transcend some of the more deep-seated obstacles associated with entrepreneurship, while saying what aspects of interventions are still lacking in order to realize their full potential. The findings are meant to deepen the understanding of the intersection between gender, technology, and entrepreneurship in Africa; as such, they need to provide actionable recommendations on ways to foster an inclusive digital economy.

Methodology

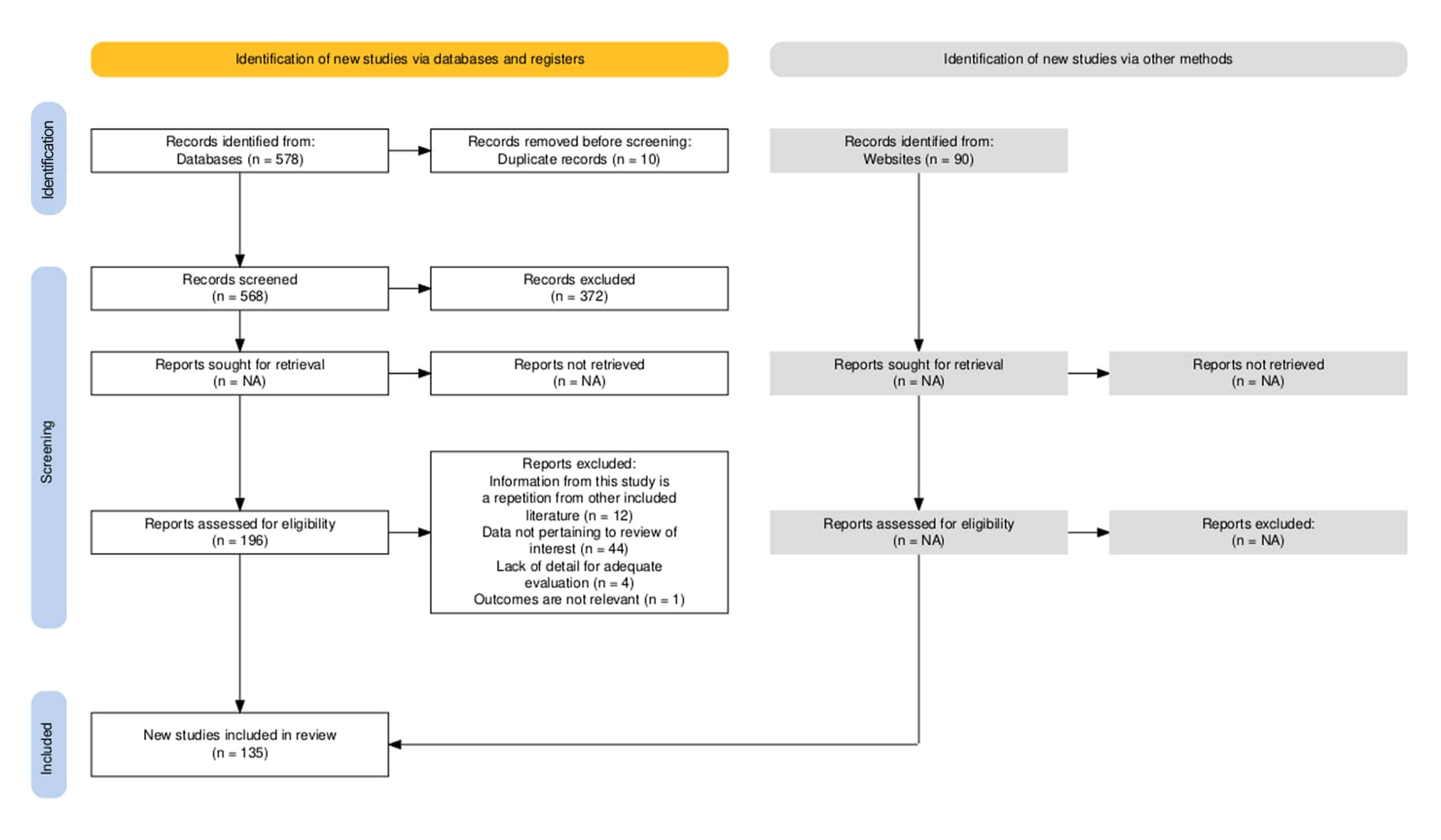

Study design: This review integrates both quantitative and qualitative data from existing literature on female entrepreneurship in Africa, primarily on e-commerce, fintech, and agritech sectors. The present study aims to ascertain how these digital platforms are changing the face of female entrepreneurship and to identify the main challenges faced by females in adopting and using such technologies. This systematic review followed the preferred reporting items for systematic reviews and meta-analyses (PRISMA) guidelines, and a predefined protocol was registered with PROSPERO, outlining the review objectives, inclusion/exclusion criteria, and data extraction processes.

Data sources: The paper obtained its academic literature, reports, and studies from the following databases: Google Scholar, JSTOR, Science Direct, World Bank Reports, and African Development Bank Reports. In addition to peer-reviewed articles, grey literature such as policy briefs, non-governmental organization (NGO) reports, and case studies from relevant African organizations and incubators were included. Grey literature was included only if it met predefined quality criteria, ensuring it was reliable and relevant to the review.

| Domain | Details |

| Databases | Google Scholar, JSTOR, Science Direct, World Bank Reports, African Development Bank Reports |

| Grey literature | Policy briefs, NGO reports, case studies from African organizations and incubators (included if meeting quality criteria) |

| Search terms | “Female entrepreneurship in Africa,” “Digital technologies and African women,” “E-commerce and women entrepreneurs in Africa,” “Fintech platforms in Africa,” “Agritech women entrepreneurs in Africa,” “Financial inclusion for African women” |

| Publication dates | 2010-2023 |

| Inclusion criteria | Academic literature and grey literature relevant to female entrepreneurship and digital platforms in Africa |

| Exclusion criteria | Studies not focused on Africa, not related to female entrepreneurship or digital platforms, or published before 2010 |

Table 1: Summary of search results for the database

Search strategy: The search strategy involved using specific keywords related to the research question. The primary search terms included: “Female entrepreneurship in Africa”, “Digital technologies and African women”, “E-commerce and women entrepreneurs in Africa”, “Fintech platforms in Africa”, “Agritech women entrepreneurs in Africa”, “Financial inclusion for African women”. The search was limited to publications between 2010 and 2023 to focus on the most recent developments in digital technologies and entrepreneurship in Africa.

Inclusion criteria: 1) Studies on female entrepreneurship in Africa, 2) Studies focusing on e-commerce, fintech, or agritech platforms, 3) Quantitative, qualitative, and mixed methods studies, and 4) Publications in English from 2010-2023.

Exclusion criteria: 1) Studies not focused on digital technologies, 2) Studies outside Africa, and 3) Publications before 2010, or not in English.

The search strategy used was: (‘Female entrepreneurship’ AND ‘Africa’) AND (‘e-commerce’ OR ‘fintech’ OR ‘agritech’), limited to English-language publications between 2010 and 2023. The literature search was conducted between January 2023 and March 2023.

| Domain | Inclusion criteria | Exclusion criteria |

| Study design | Quantitative, qualitative, and mixed methods studies related to female entrepreneurship in Africa | Studies not focused on digital technologies or those outside Africa |

| Participants | Studies focused on female entrepreneurs in Africa | Studies not focused on female entrepreneurship |

| Exposures | Digital technologies such as e-commerce, fintech, and agritech platforms used by female entrepreneurs | Studies that do not focus on e-commerce, fintech, or agritech platforms |

| Comparators | N/A (No explicit comparators mentioned in the methodology) | N/A |

| Outcomes | Financial inclusion, market access, business growth, access to finance, digital literacy challenges | Outcomes unrelated to digital technologies or female entrepreneurship |

| Timing | Studies published between 2010 and 2023 | Publications before 2010 or not in English |

| Setting | Studies conducted in Africa, including digital platforms like Jumia, M-Pesa, and FarmDrive | Studies conducted outside Africa |

Table 2: Inclusion and exclusion criteria

Data extraction and synthesis: This review employed narrative synthesis to integrate qualitative data, organizing studies by key themes such as access to finance, digital literacy, and market access. Quantitative results, where available, were synthesized using a meta-analysis approach. After collecting relevant studies, data were extracted using a structured format to capture essential information, including Country of study, Digital platform(s) discussed (e.g., Jumia for e-commerce, M-Pesa for fintech, FarmDrive for agritech), Sector of focus, Challenges identified for female entrepreneurs, and Outcomes related to financial inclusion, market access, and business growth. The qualitative data was categorized to identify common themes such as access to finance, digital literacy challenges, market expansion, and the gender digital divide. Quantitative data, such as growth rates of women-owned tech startups and the percentage of female participation in these sectors, were compiled to assess the overall impact of digital technologies.

Quality assessment: The quality of included studies was assessed using the Newcastle-Ottawa scale for non-randomized studies and the Cochrane risk of bias tool for randomized controlled trials. Two independent reviewers conducted the study screening and selection. Discrepancies were resolved through discussion or a third reviewer.

Results

Figure 1: PRISMA flow chart

Role of e-commerce in expanding market access: E-commerce and digital marketing enable businesses to expand their target market, increase sales, and improve customer communication, with digitalization accelerating due to the COVID-19 pandemic.[5] About 51% of sellers on Jumia in Kenya and Nigeria are female entrepreneurs.[1] E-commerce platforms and social networking have significantly influenced consumer marketing strategies, enabling businesses to better understand consumer needs and share innovative information in a competitive global environment.[6] E-commerce is a crucial tool for businesses, allowing them to reach more customers and effectively market their products in today’s volatile market conditions.[5]

How platforms like Jumia, Takealot, and social media have allowed women to reach new markets: Social media entrepreneurship offers women in Tunisia new opportunities for business, but formalization remains a challenge due to the informal nature of Facebook-commerce businesses.[7] 40% of women-owned businesses on e-commerce platforms experienced revenue growth during the pandemic compared to 26% of offline businesses.[3] Social media is crucial for women entrepreneurs in the national capital region (NCR) to connect with customers, promote their businesses, and develop skills, despite a conservative culture.[8] Social media platforms enable women entrepreneurs in Southern Philippines to start or continue their businesses, expand their market reach, and express autonomy through innovative use of features.[9] 75% of female entrepreneurs rely on mobile phones for business operations, with 45% using social media for direct sales.[2] Jordanian women entrepreneurs using social media as their primary business platform experience varying degrees of empowerment and economic gains, with empowerment influenced by their motivations for entrepreneurship.[10]

Case studies of successful female entrepreneurs

- Rebecca Enonchong (Cameroon) – Fintech: Founder and CEO of AppsTech, Rebecca Enonchong expanded her enterprise globally using digital technologies. As a co-founder of the African business angel network (ABAN), she supports female entrepreneurs in the African tech space. Her success exemplifies how fintech innovations can help women access global markets and navigate funding challenges.[11]

- Nthabiseng Mosia (South Africa) – Agritech: Co-founder of Easy Solar, Mosia provides solar energy to off-grid communities in Sierra Leone. By integrating mobile payments, she enables women to manage small businesses, contributing to economic empowerment and sustainability in rural areas.[12]

- Funke Opeke (Nigeria) – E-Commerce & Fintech: As the founder of MainOne, Opeke revolutionized broadband access in West Africa, empowering Nigerian women entrepreneurs to utilize e-commerce and fintech platforms. Her work highlights the importance of infrastructure in digital entrepreneurship.[13]

- Fatoumata Ba (Senegal) – E-Commerce: Founder of Jumia Ivory Coast and Janngo Capital, Ba expanded Jumia’s reach and provided opportunities for thousands of African women to sell products online. She focuses on empowering female-led startups through digital platforms.[14]

The analysis of e-commerce platforms such as Jumia and Takealot reveals a notable increase in market access for female entrepreneurs across Africa. Studies show that about 51% of sellers on these platforms in Kenya and Nigeria are women, indicating a significant shift in market dynamics.[1] However, challenges such as limited internet access in rural areas still restrict the full potential of e-commerce for many women.[5] This divergence suggests that while urban entrepreneurs are thriving, rural women continue to face substantial barriers to digital entrepreneurship.

Challenges in e-commerce

Issues like limited digital literacy and internet access: Agribusiness can gain a competitive advantage by deploying e-commerce technologies, overcoming technical, government policy, and legal challenges.[15] Training programs for regional SMEs enhance their digital literacy awareness, knowledge, and skills, fostering confidence in digital technologies for entrepreneurial advancement.[16] B2B e-commerce faces challenges in technology adoption, information sharing, and financial returns, but addressing these issues can lead to greater success.[17] Cross-border e-commerce faces challenges such as logistics, language, legal regulation, and geo-blocking, hindering its integration into a fully integrated digital market.[18] Widespread internet access benefits citizens and businesses, but also presents challenges in digital literacy and network power, requiring policies to promote both.[19]

Findings and analysis: The analysis of e-commerce platforms such as Jumia and Takealot reveals a notable increase in market access for female entrepreneurs across Africa. Studies show that about 51% of sellers on these platforms in Kenya and Nigeria are women, indicating a significant shift in market dynamics.[1] However, challenges such as limited internet access in rural areas still restrict the full potential of e-commerce for many women.[5] This divergence suggests that while urban entrepreneurs are thriving, rural women continue to face substantial barriers to digital entrepreneurship.

Impact of fintech on financial inclusion: The use of platforms like M-Pesa, Paga, and digital wallets plays a crucial role in overcoming financial exclusion by providing accessible and convenient financial services to individuals who are unbanked or underbanked. M-Pesa in Kenya promotes social entrepreneurship, but its focus on opportunity rather than redistribution may not benefit the unbanked poor.[20] The 40% of M-Pesa’s users are women, with 30% of these users utilizing the platform for business transactions.[2] Fintech innovations significantly drive financial inclusion and empowerment by providing affordable and convenient financial services to underserved populations, promoting entrepreneurship, and economic growth.[21]. Fintech usage positively impacts financial inclusion, but the digital divide moderates its impact, with performance expectancy and facilitating conditions playing key roles in behavioral intentions.[22] Digital wallet adoption is influenced by perceived usefulness, price value, and trust, which can promote greater financial inclusion among disadvantaged and low-income individuals.[23] Fintech reduces income inequality through financial inclusion, primarily in higher-income countries, supporting the United Nations-2030-agenda for sustainable development (UN-2030-ASD) and G20 high-level principles for digital financial inclusion (G20-HLP-DFI) aspirations(Demir et al., 2022).

Case studies highlight the role of fintech in providing microloans, savings options: Fintech innovations significantly drive financial inclusion and empowerment by providing affordable and convenient financial services to underserved populations, promoting entrepreneurship, and economic growth.[21] Women-led businesses on digital lending platforms like M-Pesa received microloans 20% faster than through traditional banks, with loan sizes averaging 15% smaller. Fintech-based financial inclusion reduces the risk-taking behavior of Sub-Saharan African microfinance institutions.[24]

Challenges in fintech

Difficulties in accessing large-scale funding, gender-based financial biases: Fintech technologies significantly impact access to finance for firms and investors, but face regulatory challenges and require further research.[25] Only 10% of venture capital in Africa is allocated to female-led startups, despite a 15% annual increase in women-owned fintech businesses. SMEs in the democratic republic of Congo face constraints in accessing finance due to lack of collateral, high interest rates, and inability to develop attractive projects, but both women and men have equal chances of accessing finance.[26] The fintech gender gap exists, with 29% of men using fintech products and services, while only 21% of women do, with country characteristics and individual-level controls explaining a third of the gap.[27] Gender influences the signals communicated in entrepreneur-investor relationships, potentially contributing to gender biases in risk capital investments.[28]

Findings and analysis: In Sub-Saharan Africa, m-Pesa in Kenya has contributed significantly to women’s financial inclusion, with almost 40% of users being women.[2] However, this ignores marginalised sections and particularly rural areas that are still unable to avail themselves of such financial services due to the lack of infrastructure.[20] These differences indicate that although Fintech is disruptive in bringing change, the change does not reach everyone. This, in turn, implies that there should be strategies that direct efforts towards overcoming the digital gap in distant areas.

Agricultural innovations through agritech

Role of platforms like FarmDrive and Esoko in improving agricultural practices for women: AI-driven AgriTech research is in its infancy, but its potential for smart, efficient, and sustainable farming is growing rapidly (Spanaki et al., 2022). 30% of rural women farmers use agritech tools, with 50% of them reporting increased productivity after adopting platforms like FarmDrive (Spanaki et al., 2022). A gender-responsive approach is crucial for the successful adoption of digital agriculture technologies by farmers, especially women, requiring multistakeholder partnerships and responsible research and innovation (Jarial & Sachan, 2021). Women’s participation in agricultural cooperatives, entrepreneurship, access to land rights, and extension services positively influences agricultural productivity and income generation (Chebet, 2023). Farmers’ initial acceptance of a mobile digital platform for farm management is shaped by social influence, performance, and effort expectancy, and trust beliefs, while continued use is influenced by performance, effort expectancy, trust beliefs, and perceived work impediment (Fox et al., 2021). New-ICT platforms in Ghana’s agricultural extension service are aimed at supporting innovation-intermediation roles, but their potential is hindered by social, organizational, and institutional factors (Munthali et al., 2018).

How women farmers are using these platforms for better market access and supply chain management: AI-driven AgriTech research is in its infancy, but its potential for smart, efficient, and sustainable farming is growing rapidly (Spanaki et al., 2022). About 35% of agritech users in rural Africa rely on mobile wallets to receive payments, ensuring better financial inclusion (OECD, 2018). The 4.0 technologies enable open innovation and shared value creation in agrifood businesses, while reducing resource waste and enhancing supply chain sustainability (Rialti et al., 2022). The 60% of female farmers using Esoko improved their crop yields and market prices through real-time data updates (Chilundo et al., 2020). Innovation platforms can improve rural women’s participation in the maize value chain, with the main effect being improved market access rather than increased maize yields (Mumbeya et al., 2020).

Challenges in agritech

Barriers like lack of digital literacy and land ownership: Gendered land distribution in South Africa contributes to food insecurity, with customary law hindering women’s equal access to land ownership compared to men.[29] A gender-responsive approach is crucial for the successful adoption of digital agriculture technologies by farmers, especially women, requiring multistakeholder partnerships and responsible research and innovation.[30] Smallholder agricultural programs targeted at rural black and colored South African women can stimulate awareness of possibilities, visions, ownership, and rights, but face operational challenges and a lack of financial sustainability.[31] Inadequate financial support, excessive post-harvest loss, gender inequality, non-climate-smart policies, and weak institutional controls are major barriers to sustainable agribusiness success.[32]. Lack of education, family pressures, and discrimination hinder the success of women entrepreneurs in developing countries like King Williams’ Town, South Africa.[33]

Findings and analysis: Despite the increasing presence of female entrepreneurs in fintech, a significant gender gap persists in venture capital allocation. Some studies highlight a 15% annual increase in women-owned fintech businesses, but only 10% of venture capital is directed toward female-led startups. This contradiction points to a systemic bias in funding, which stifles the potential for women to scale their businesses. Addressing this gender gap will be critical in ensuring equal opportunities for female entrepreneurs in Africa’s digital economy.

Identifying gaps in research–Agritech: While agritech platforms like FarmDrive have demonstrated success in improving agricultural productivity for women, with 50% of users reporting increased crop yields, there is a notable gap in studies exploring the long-term impact of these technologies on financial sustainability and land ownership.[34] This absence in the literature highlights the need for more comprehensive research that addresses systemic issues such as gender-based land distribution, which continues to limit the economic empowerment of rural women farmers.

Challenges identified:

- Many African women, especially in rural areas, struggle with access to smartphones, the internet, and digital tools, crucial for e-commerce, fintech, and agritech. Women are 20% less likely to own smartphones or access the internet compared to men.

- Most women lacked advanced skills in website management, digital marketing, and data analysis, which are key in scaling businesses. The absence of exposure to education in science, technology, engineering, and mathematics (STEM) widens this gap in skills and hampers women from harnessing technology effectively.

- The women-led ventures in the areas of fintech and agritech are most affected. Although there has been some improvement in microfinance, venture capital investment in female startups remains low, limiting the potential of women to scale up and innovate.

Recommendations

- The government and NGOs should make collaborative efforts on basic and advanced digital skills training programs, including social media marketing, e-commerce management, fintech, and agritech tools.

- There is a need to make opportunities for using digital resources available by providing subsidies on smartphones and internet services, or offering free Wi-Fi. Collaboration with financial institutions provides incentives to women-led startups, promotes STEM participation since increased involvement in digital entrepreneurship sets it higher in the long run.

- Expand microfinance programs and establish venture capital funds that target women entrepreneurs. Provide alternative credit scoring using e-commerce data by governments and Fintech platforms to limit gender biases in lending and increase access to capital.

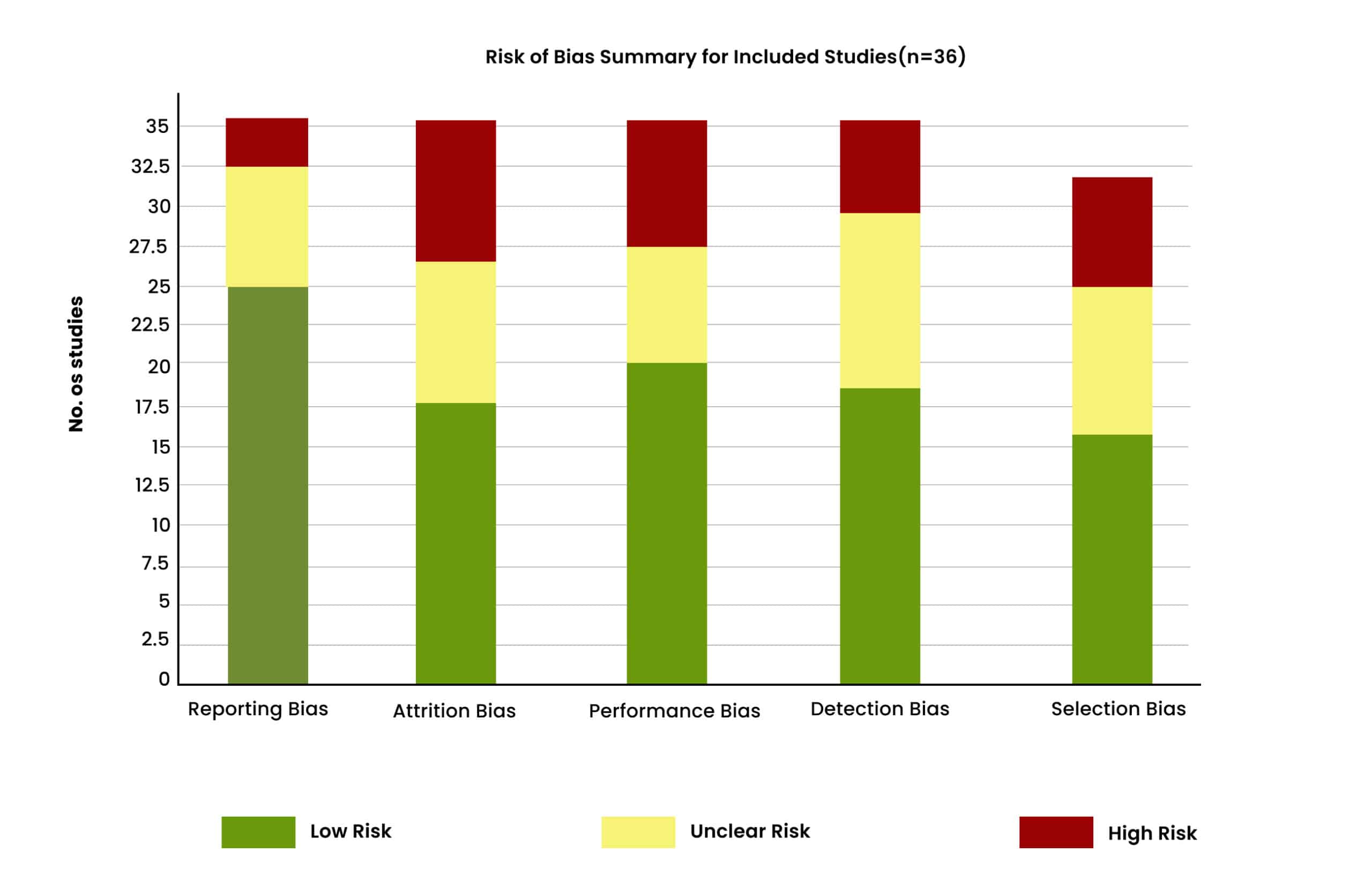

Figure 2: Risk of bias assessment

Figure 2 illustrates the distribution of the studies according to the different bias types: low risk, unclear risk, and high risk with respect to selection, performance, detection, attrition, and reporting bias.

Limitations: The language with non-English publications is likely to be excluded, selection bias due to the fact that only peer-reviewed articles were relied upon, and absence of a meta-analytic procedure due to the implausibility of the availability of consistent data across clips.

Conclusion

The advent of technologies, especially through the provision of integrated digital platforms such as e-commerce, fintech, and agritech solutions, has enabled many women entrepreneurs in Africa to thrive. Paradoxically, what is apparent in almost all the studies is the widespread regional disparity in technology penetration, especially among women entrepreneurs in rural areas, as well as gender discrimination in access to finance and venture capital. Targeting these ingrained, systemic barriers through purposeful policy and investment will be an important aspect of harnessing the opportunities that come with the digital economy among women. This systematic review shows that digital technologies are rapidly changing the face of female entrepreneurship in Africa, especially in e-commerce, fintech, and agritech. Such platforms have enabled women to break through traditional barriers in the form of limited mobility, financial exclusion, and restricted access to markets. A host of challenges remain, however, with regard to the gendered digital divide, lack of higher-order digital skills, and impediments to funding access that hamper the full power of such innovations. This would involve specific interventions in the form of programs on digital literacy, gender-inclusive policies, and innovative models of finance targeting women entrepreneurs. A collaborative approach wherein governments, NGOs, financial institutions, and private sector partners come together could help Africa achieve an inclusive digital economy that empowers women for sustainable growth. These efforts could unlock the radical and political potential of digital technologies and promote economic progress while reducing gender inequalities across the continent. In order to circumvent the obstacles identified in this review, there is a pressing urgency for policies and programs that seek to bridge the rural-urban disparity in technological access and adoption, as well as policies that promote the role of women in financing. Recommended actions include making available digital literacy programs adapted to the needs of rural women and creating venture capital facilities that focus on female entrepreneurs.

References

- International Finance Corporation (IFC). Women and E-Commerce in Africa. 2021. Women and E-Commerce in Africa

- World Bank Group. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution (English). 2018. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution (English)

- Donor Committee for Enterprise Development (DCED). Bridging the Digital Gender Divide: Include, upskill, innovate – OECD (2018). 2018. Bridging the Digital Gender Divide: Include, upskill, innovate – OECD (2018)

- Spanaki K, Sivarajah U, Fakhimi M, Despoudi S, Irani Z. Disruptive technologies in agricultural operations: a systematic review of AI-driven AgriTech research. Ann Oper Res. 2022;308(1-2):491-524. doi:10.1007/s10479-020-03922-z Crossref | Google Scholar

- Turchyn L, Kunešová H. E-commerce as a modern paradigm of formation and use of marketing tools. Trendy v Podnikání. 2022;12(2):88-100. doi:10.24132/jbt.2022.12.2.88_100 Crossref

- Rosário A, Raimundo R. Consumer marketing strategy and e-commerce in the last decade: a literature review. J Theor Appl Electron Commer Res. 2021;16(7):3003-3024. doi:10.3390/jtaer16070164 Crossref | Google Scholar

- Brahem M, Boussema S. Social media entrepreneurship as an opportunity for women: the case of Facebook-commerce. Int J Entrep Innov. 2023;24(3):191-201. doi:10.1177/14657503211066010 Crossref | Google Scholar

- Kataria DK, Phukan DR. Social media and digital marketing of women entrepreneurs in NCR. Veethika Int Interdiscip Res J. 2022;8(4):9-15. doi:10.48001/veethika.2022.08.04.002 Crossref | Google Scholar

- Lavilles R, Tinam-Isan MA, Sala EL. Social media as an enabler of women’s entrepreneurial empowerment during the pandemic. Asian J Women Stud. 2023;29(1):136-153. doi:10.1080/12259276.2023.2186633 Crossref | Google Scholar

- Boshmaf H. Jordanian women entrepreneurs and the role of social media: the road to empowerment. Dirasat Hum Soc Sci. 2023;50(3):139-152. doi:10.35516/hum.v50i3.5402 Crossref | Google Scholar

- Chebet N. The role of women on agricultural sector growth. Int J Agric. 2023;8(1):41-50. doi:10.47604/ija.1980

Crossref | Google Scholar - Fox G, Mooney J, Rosati P, Lynn T. AgriTech innovators: a study of initial adoption and continued use of a mobile digital platform by family-operated farming enterprises. Agriculture. 2021;11(12):1283. doi:10.3390/agriculture11121283 Crossref | Google Scholar

- Rialti R, Marrucci A, Zollo L, Ciappei C. Digital technologies, sustainable open innovation and shared value creation: evidence from an Italian agritech business. Br Food J. 2022;124(6):1838-1856. doi:10.1108/BFJ-03-2021-0327

Crossref | Google Scholar - Mbeteh A, Pellegrini MM. An integrated framework of entrepreneurial competencies and pedagogical approaches in Sierra Leone. In: Mbeteh A, Pellegrini MM, eds. Entrepreneurship Education in Africa: A Contextual Model for Competencies and Pedagogies in Developing Countries. Emerald Publishing Limited; 2022:89-106. doi:10.1108/978-1-83909-702-720221010 Crossref | Google Scholar

- Rao NH. Electronic commerce and opportunities for agribusiness in India. Outlook Agric. 2003;32(1):29-33. doi:10.5367/000000003101294235 Crossref | Google Scholar

- Ollerenshaw A, Corbett J, Thompson H. Increasing the digital literacy skills of regional SMEs through high-speed broadband access. Small Enterp Res. 2021;28(2):115-133. doi:10.1080/13215906.2021.1919913 Crossref | Google Scholar

- Dai Q, Kauffman RJ. B2B e-commerce revisited: leading perspectives on the key issues and research directions. Electron Mark. 2002;12(2):67-83. doi:10.1080/10196780252844517 Crossref | Google Scholar

- Kalinić Z, Ranković V, Kalinić L. Challenges in cross-border e-commerce in the European Union. Zesz Nauk UE Krakowie. 2019;5(977):159-170. doi:10.15678/ZNUEK.2018.0977.0510 Crossref | Google Scholar

- Silva EC. Social and political challenges of the Digital Single Market and of increasing connectivity: digital literacy and network power. UNIO – EU Law J. 2018;4(2):33-41. doi:10.21814/unio.4.2.4 Crossref | Google Scholar

- Natile S. Regulating exclusions? Gender, development, and the limits of inclusionary financial platforms. Int J Law Context. 2019;15(4):461-478. doi:10.1017/S1744552319000417 Crossref | Google Scholar

- Geetha, Kalaiselvi. Impact of fintech innovations: expanding access and empowering communities. Int J Multidiscip Res. 2023;5(5):7518. doi:10.36948/ijfmr.2023.v05i05.7518 Crossref

- Odei-Appiah S, Wiredu G, Adjei JK. Fintech use, digital divide, and financial inclusion. Dig Policy Regul Gov. 2022;24(5):435-448. doi:10.1108/DPRG-09-2021-0111 Crossref | Google Scholar

- Shrestha R, Tamang L. Financial inclusion through fintech innovation: predicting user acceptance of digital wallet. The Batuk. 2023;9(2):37-48. doi:10.3126/batuk.v9i2.57026 Crossref | Google Scholar

- Banna H, Mia MA, Nourani M, Yarovaya L. Fintech-based financial inclusion and risk-taking of microfinance institutions (MFIs): evidence from Sub-Saharan Africa. Finance Res Lett. 2022;45:102149. doi:10.1016/j.frl.2021.102149

Crossref | Google Scholar - Bollaert H, Lopez-de-Silanes F, Schwienbacher A. Fintech and access to finance. J Corp Finance. 2021;68:101941. doi:10.1016/j.jcorpfin.2021.101941 Crossref | Google Scholar

- Woldie A, Mwangaza Laurence B, Thomas B. Challenges of finance accessibility by SMEs in the Democratic Republic of Congo: is gender a constraint? Invest Manag Financ Innov. 2018;15(2):40-50. doi:10.21511/imfi.15(2).2018.04

Crossref | Google Scholar - Shin HS, Gambacorta L, Frost J, Doerr S, Chen S. The fintech gender gap. SSRN Electron J. 2021. doi:10.2139/ssrn.3799864 Crossref | Google Scholar

- Alsos GA, Ljunggren E. The role of gender in entrepreneur-investor relationships: a signaling theory approach. Entrep Theory Pract. 2017;41(4):567-590. doi:10.1111/etap.12226 Crossref | Google Scholar

- Masuku MM, Mthembu Z, Mlambo VH. Gendered effects of land access and ownership on food security in rural settings in South Africa. Front Sustain Food Syst. 2023;7:1158946. doi:10.3389/fsufs.2023.1158946 Crossref | Google Scholar

- Jarial S, Sachan S. Digital agriculture through extension advisory services: is it gender-responsive? A review. Int J Agric Ext. 2021;9(3):559-566. doi:10.33687/ijae.009.03.3687 Crossref | Google Scholar

- Lemke S, Yousefi F, Eisermann A, Bellows A. Sustainable livelihoods approaches for exploring smallholder agricultural programs targeted at women: examples from South Africa. J Agric Food Syst Community Dev. 2012;25-41. doi:10.5304/jafscd.2012.031.001 Crossref | Google Scholar

- Brenya R, Akomea-Frimpong I, Ofosu D, Adeabah D. Barriers to sustainable agribusiness: a systematic review and conceptual framework. J Agribus Dev Emerg Econ. 2023;13(4):570-589. doi:10.1108/JADEE-08-2021-0191

Crossref | Google Scholar - Mandipaka F. An investigation of the challenges faced by women entrepreneurs in developing countries: a case of King Williams’ Town, South Africa. Mediterr J Soc Sci. 2014. doi:10.5901/mjss.2014.v5n27p1187 Crossref | Google Scholar

- Spanaki K, Sivarajah U, Fakhimi M, Despoudi S, Irani Z. Disruptive technologies in agricultural operations: a systematic review of AI-driven agritech research. Ann Oper Res. 2022;308(1–2):491-524. doi:10.1007/s10479-020-03922-z

Crossref | Google Scholar

Acknowledgments

Not reported

Funding

Not reported

Author Information

Muhammad Ahsan Fayyaz

Department of Dentistry

Institute of Dentistry, CMH Lahore Medical College, Pakistan

Email: ahsanfayyaz981@gmail.com

Author Contribution

The author contributed to the conceptualization, investigation, and data curation by acquiring and critically reviewing the selected articles, and was involved in the writing – original draft preparation and writing – review & editing to refine the manuscript.

Ethical Approval

Not applicable

Conflict of Interest Statement

Not reported

Guarantor

None

DOI

Cite this Article

Muhammad AF. The Transformative Role of Digital Technologies in Female Entrepreneurship in Africa: A Focus on E-Commerce, Fintech, and Agritech. medtigo J Pharmacol. 2024;1(1): e3061123. doi:10.63096/medtigo3061123 Crossref